written by by Gregg Early, BankTalentHQ

Let’s not talk about the past year.

Let’s take the long view and talk about the past decade and a half.

For nearly all of that time we lived in a “next normal” of quantitative easing, which brought along with it easy money and sustained low interest rates.

It was a bit of shock to begin with, like inducing a coma to save a patient. But after a while, as it always does, the market finds a way to turn challenges into opportunities.

The pandemic changed all the math once again, transitioning from an induced coma to popping out of bed and running an Iron Man competition.

Pivoting to the Next Next Normal

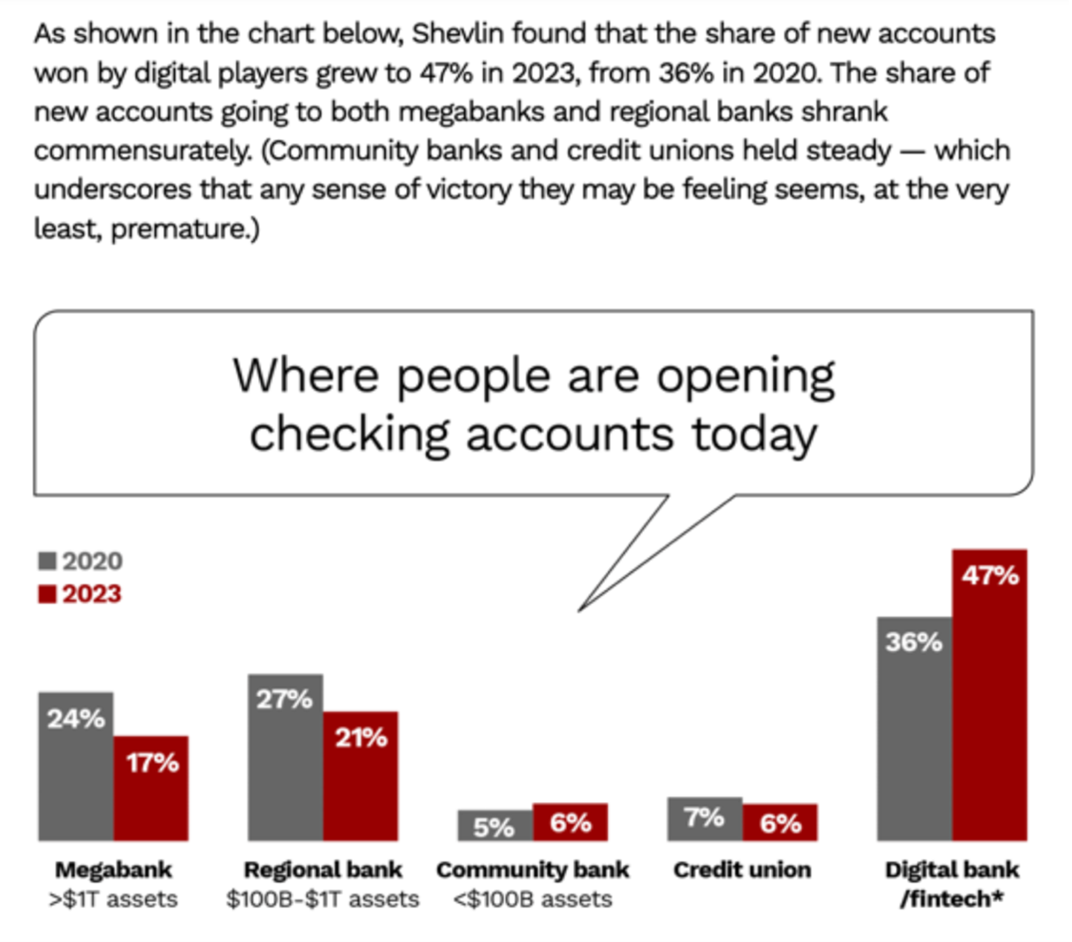

And that flood of even more cash certainly helped community banks’ and credit unions’ competitors – the megabanks and the VC-infused fintechs and neobanks.

It’s still rippling through the financial community today.

Source: Financial Brand

Two Goliaths are now on community FIs’ doorstep.

Many community FIs looked to fight fire with fire and expand their acquisition strategies. But the reality is, only ~11% of accounts are even interested in moving their primary accounts and more than half of those are going the wrong way – from community FIs to megabanks.

What’s more, an acquisition strategy is expensive. And even the megabanks are now realizing hat winning the deposit war early on is becoming a somewhat pyrrhic victory.

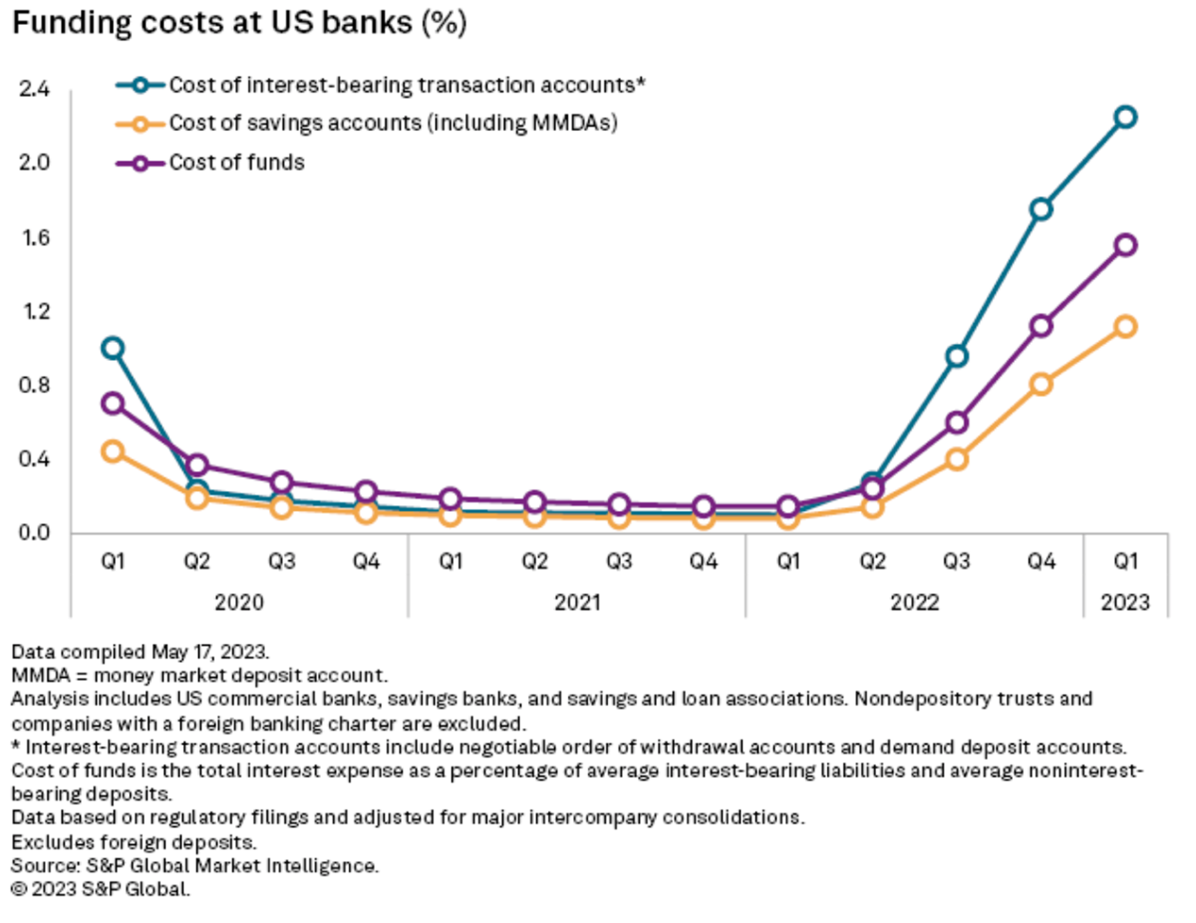

Net interest margin is falling and is expected to continue to fall as interest rates stabilize and servicing all those new consumer accounts at high interest rates becomes more expensive, especially as interest rates start to recede later this year or next year.

Source: Forbes

Source: Forbes

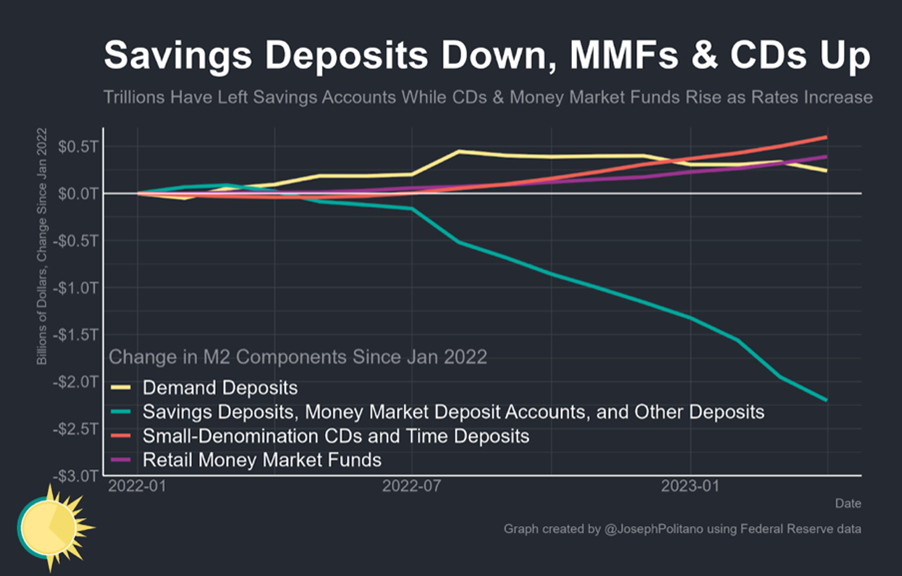

Add to that the fact that consumer demand deposit accounts are drying up as inflation continues to erode consumers’ spending power and the money they had piled up before and during the pandemic is ebbing or moving to money markets and CDs that deliver higher interest rates.

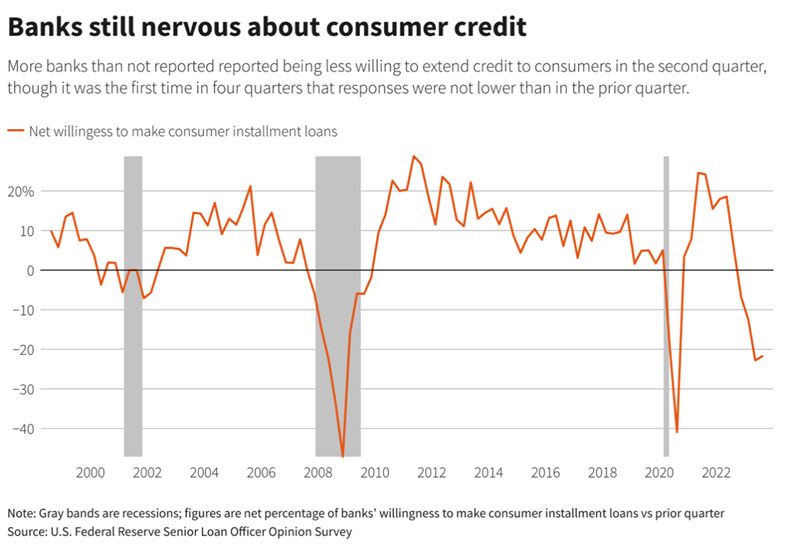

Plus, the credit markets are drying up for both consumer and commercial loans as all FIs begin to enforce tighter credit standards.

So, FIs are in the midst of a 1-2 punch combination – plummeting deposits, as well as shrinking loan books for consumers and business accounts.

While a majority of the loan business already has been going to the megabanks and fintechs up to now due to their ability to offer the best DDA rates, as they add these borrowers, they’re also adding to their risks of defaults if economic conditions deteriorate. This is especially true of the fintechs since their business models are still relatively young and unproven in challenging markets.

Don’t Knock the Slingshot

So, where do community FIs turn in such a difficult market with competition coming from all sides?

Well, broadly speaking the first place to look isn’t outward, but inward.

Conveniently for every FI looking at an acquisitive marketing strategy, organically growing business is much less expensive and yields much better results than hunting down new customers/members.

This is great news for community FIs, because their strengths have always been to deliver more personalized service in a local or regional market that they understand deeply.

What’s more, this is the trusty slingshot community Davids can use against the industry Goliaths.

Relationship Banking 2.0

While the megabanks and fintechs scramble to find ways to keep their customers, community FIs are well positioned to grow their base organically and deliver the kind of banking experiences that have kept them thriving for decades.

Creating value for customers and members with valuable products that help consumers centralize their financial lives in one place will boost non-interest income and grow primary accounts.

The current environment may seem dire for community FIs some days. But it’s possible to reframe current conditions to see the inherent opportunities they provide for community FIs.

One of the first steps is to stop thinking like a giant and relish the unique, creative opportunities community FIs can provide for their customers and members without going toe-to-toe with megabanks.

For two decades StrategyCorps has worked with financial institutions nationwide to deliver top-performing retail checking analytical and product solutions (and recently small business checking solutions) – the foundation of all banking relationships. Using proprietary analytics to identify primary and non-primary accounts, StrategyCorps then designs and builds checking products with non-traditional banking services that save customers money when they spend it on everyday necessities and protect their important assets. The payoff to clients is boosting primacy and growing deposits and non-interest income, while also standing out from the crowd of basic checking account services.

Gregg Early is a financial writer and editor who’s worked as a journalist for American Banker, Bond Buyer, and others covering the SEC, MSRB, Supreme Court, and various Congressional finance committees. His expertise is fintech, emerging technologies, biotech, ESG, green tech, cryptocurrencies and derivatives. His work has been featured on CNBC, CNN, and Bloomberg, as well as in The New York Times, Washington Post, Wall Street Journal, and Businessweek. Contact him at gregg.early@strategycorps.com.